Utah Realty Blog & News

The Latest news for Real Estate both local and National.

Buyers

Sellers

Seniors

What’s Ahead for Mortgage Rates and Home Prices?

Now that the end of 2022 is within sight, you may be wondering what’s going to happen in the housing market next year and what that may mean if you’re thinking about buying a home. Here’s a look at the latest expert insights on both mortgage rates and home prices so you can make your best move possible.

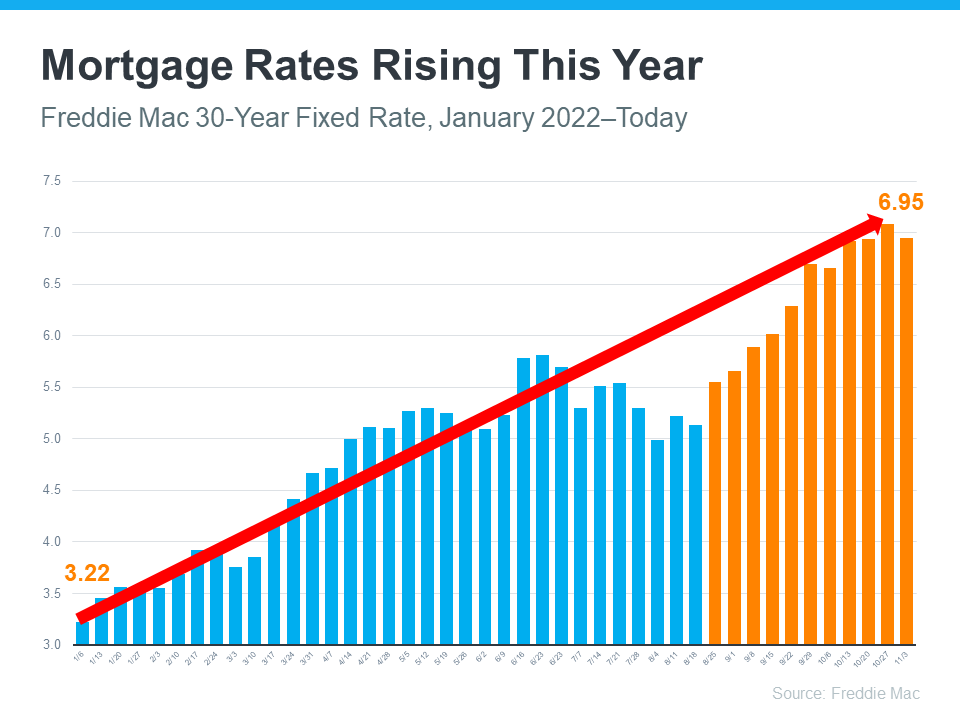

Mortgage Rates Will Continue To Respond to Inflation

There’s no doubt mortgage rates have skyrocketed this year as the market responded to high inflation. The increases we’ve seen were fast and dramatic, and the average 30-year fixed mortgage rate even surpassed 7% at the end of last month. In fact, it’s the first time they’ve risen this high in over 20 years (see graph below):

In their latest quarterly report, Freddie Mac explains just how fast the climb in rates has been:

“Just one year ago, rates were under 3%. This means that while mortgage rates are not as high as they were in the 80’s, they have more than doubled in the past year. Mortgage rates have never doubled in a year before.”

Because we’re in unprecedented territory, it’s hard to say with certainty where mortgage rates will go from here. Projecting the future of mortgage rates is far from an exact science, but experts do agree that, moving forward, mortgage rates will continue to respond to inflation. If inflation stays high, mortgage rates likely will too.

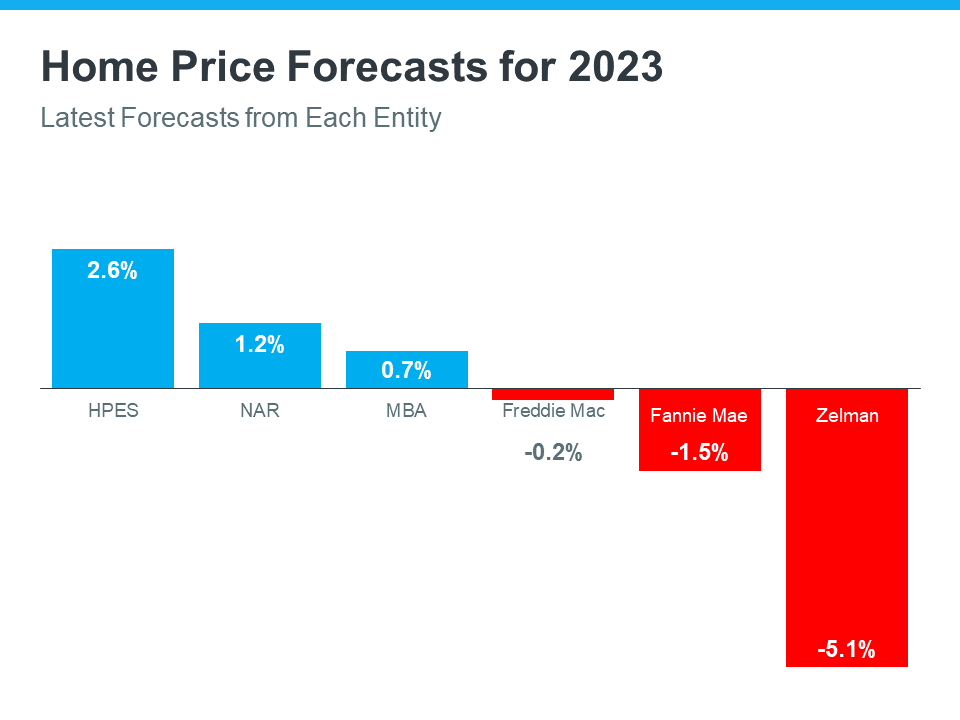

Home Price Changes Will Vary by Market

As buyer demand has eased this year in response to those higher mortgage rates, home prices have moderated in many markets too. In terms of the forecast for next year, expert projections are mixed. The general consensus is home price appreciation will vary by local market, with more significant changes happening in overheated areas. As Mark Fleming, Chief Economist at First American, says:

“House price appreciation has slowed in all 50 markets we track, but the deceleration is generally more dramatic in areas that experienced the strongest peak appreciation rates.”

Basically, some areas may still see slight price growth while others may see slight price declines. It all depends on other factors at play in that local market, like the balance between supply and demand. This may be why experts are divided on their latest national forecasts (see graph below):

Bottom Line

If you want to know what’s happening with home prices or mortgage rates, let’s connect so you have the latest on what experts are saying and what that means for our area.

Cut Your Insurance Premiums: Simple Savings Tips

Maintain a Good Credit Rating: Strong credit scores often lead to lower premiums for auto and homeowner insurance.Drive Safely: A clean driving record and good grades for students can significantly reduce insurance costs.

Utah lawmakers say no to ‘preemption,’ halt 2 housing bills aimed at allowing smaller homes

Utah lawmakers are facing challenges in addressing the housing affordability crisis, with two bills aimed at allowing smaller homes failing to progress in the legislative session. Rep. Ray Ward's proposals, which included permitting accessory dwelling units and...

Tips for Finding Bargain Houses in 2025

Start house hunting in January to benefit from lower prices and reduced buyer competition. Hire a local Real Estate agent with expertise in undervalued properties and market trends.

A Utah bill requiring 60 days notice to raise rent fails

A Utah bill requiring landlords to provide two months' notice before raising rent has been halted for the third consecutive year. The House Business, Labor, and Commerce Committee rejected HB182, which aimed to give tenants more security. The Utah Rental Housing...

Surprising Trend Pops Up in This State To Help Buyers Nab Their First Homes

A new housing trend in Utah is emerging, offering affordable options amid skyrocketing home prices, with the median list price in Salt Lake City at $550,000. Local employers are struggling to find workers due to high property costs. Homebuilder BoxHouse in St. George...

Get Your House Market-Ready

Consult a REALTOR®: A local agent helps price your home correctly and attract potential buyers. Complete Repairs: Fix any outstanding issues, like leaky faucets or worn-out flooring, for a polished look.

Join Our Newsletter

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Phasellus lacinia velit a feugiat finibus. Morbi iaculis diam id tellus iaculis, eu pretium metus fermentu