Capital gains and your home sale

When you sell your primary residence, you can make up to $250,000 in profit if you’re a single owner, twice that if you’re married, and not owe any capital gains taxes.

When the Taxpayer Relief Act of 1997 became law, the rollover or once-in-a-lifetime options were replaced with the current per-sale exclusion amounts.

You don’t have to buy another home with your sale proceeds. You can use the money as you wish.

Better yet, there’s no limit on the number of times you can use the home-sale exemption. In most cases, you can make tax-free profits of $250,000, or $500,000 depending on your filing status, every time you sell a home.

Qualifying Requirements:

- First, the property you’re selling must be your principal residence. That means you live in it. This tax break doesn’t apply to a house or other property that you have solely for investment purposes. In those cases, the usual capital gains rules apply.

- You also must live in that principal residence for 2 of the 5 years before you sell. This is known as the use test. It also means, practically speaking, each sale must be at least 2 years apart.

- That still leaves you room to make some money on several properties. You can sell your residence this year, pocket any gain within the tax limits and buy a new residence. Then 2 years later, you can do the same thing, again and again, every 2 years.

It’s just about that easy.

Shameless disclaimer: I am not a tax attorney, accountant or CPA. Always seek the property authorities for the proper

advice. Until then this will have to do.

Marty Gale

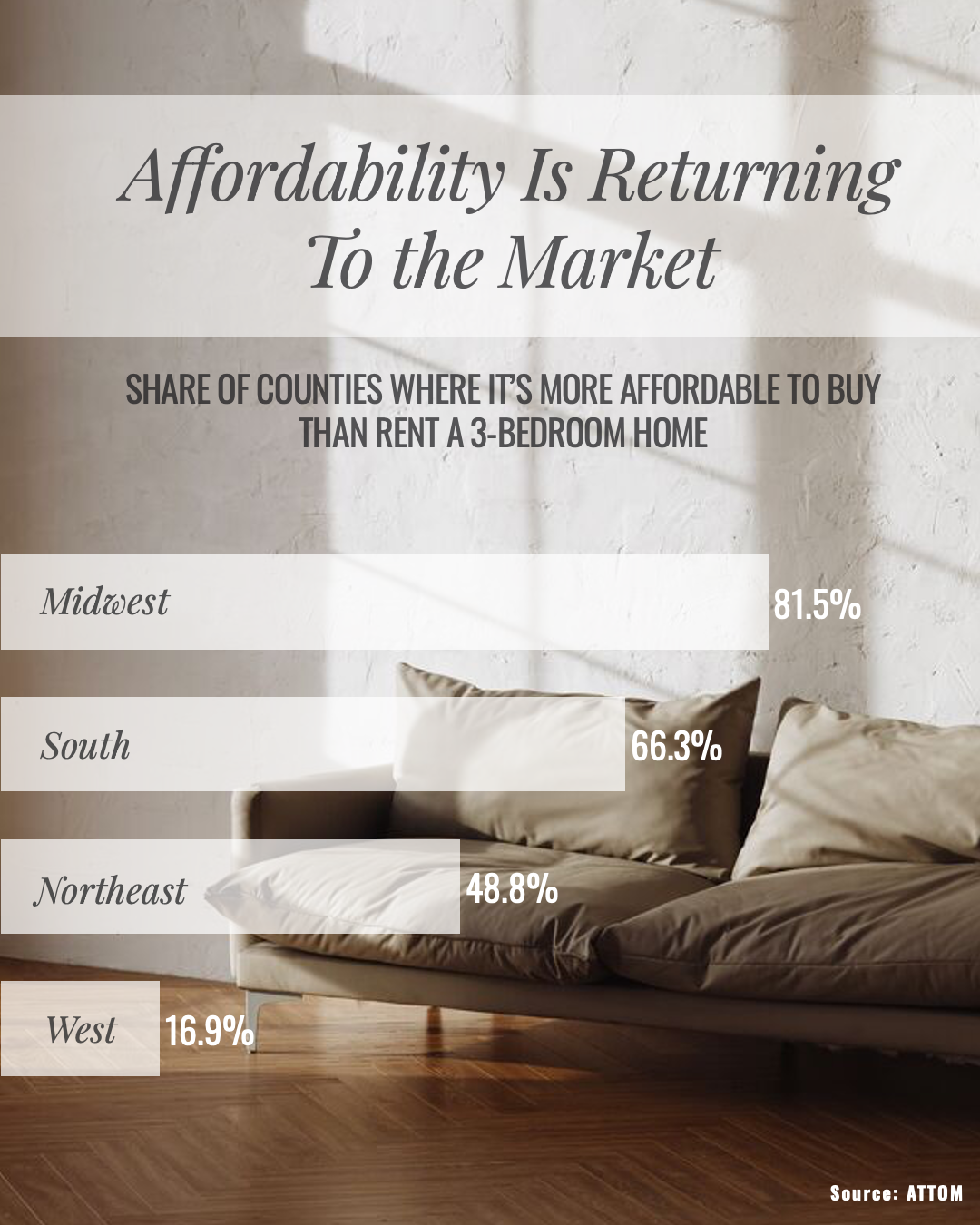

Affordability Is Returning To The Utah Market

Renting vs. Buying: The Numbers Might Surprise You Renting can feel like the easier choice right now. There’s no big down payment. No dealing with surprise repairs. And no long-term commitment. But then your rent goes up again. And again. And suddenly the thing that...

Understanding Dementia and Your Loved One

Understanding Dementia and Your Loved One Learn about their specific diagnosis (Alzheimer’s, Lewy body, vascular, frontotemporal) so expectations and plans match the condition and stage. Accept that changes in memory, behavior, and personality are caused by brain...

Top 2026 Housing Markets for Buyers and Sellers

Top 2026 Housing Markets for Buyers and Sellers Who doesn’t love a top 10 list? Well, here are two top 10 lists for the housing market this year. But before you take a look, there’s something you should know. If a move is on your radar for 2026, here’s the most...