Taking the Fear Out of the Mortgage Process

A considerable number of potential buyers shy away from the real estate market because they’re uncertain about the buying process – particularly when it comes to qualifying for a mortgage.

For many, the mortgage process can be scary, but it doesn’t have to be!

In order to qualify in today’s market, you’ll need a down payment (the average down payment on all loans last year was 5%, with many buyers putting down 3% or less), a stable income, and a good credit history.

Once you’re ready to apply, here are 5 easy steps Freddie Mac suggests to follow:

- Find out your current credit history and credit score– Even if you don’t have perfect credit, you may already qualify for a loan. The average FICO Score® for all closed loans in September was 737, according to Ellie Mae.

- Start gathering all of your documentation– This includes income verification (such as W-2 forms or tax returns), credit history, and assets (such as bank statements to verify your savings).

- Contact a professional– Your real estate agent will be able to recommend a loan officer who can help you develop a spending plan, as well as help you determine how much home you can afford.

- Consult with your lender– He or she will review your income, expenses, and financial goals in order to determine the type and amount of mortgage you qualify for.

- Talk to your lender about pre-approval– A pre-approval letter provides an estimate of what you might be able to borrow (provided your financial status doesn’t change) and demonstrates to home sellers that you’re serious about buying.

Bottom Line

Do your research, reach out to professionals, stick to your budget, and be sure you’re ready to take on the financial responsibilities of becoming a homeowner.

The House That Started It All Could Kickstart What’s Next

The House That Started It All Could Kickstart What's Next Remember how exciting it was to buy your first place? It felt like crossing a long-awaited finish line. It gave you a place to build your life. Maybe it’s where you lived when you got married. Or where you...

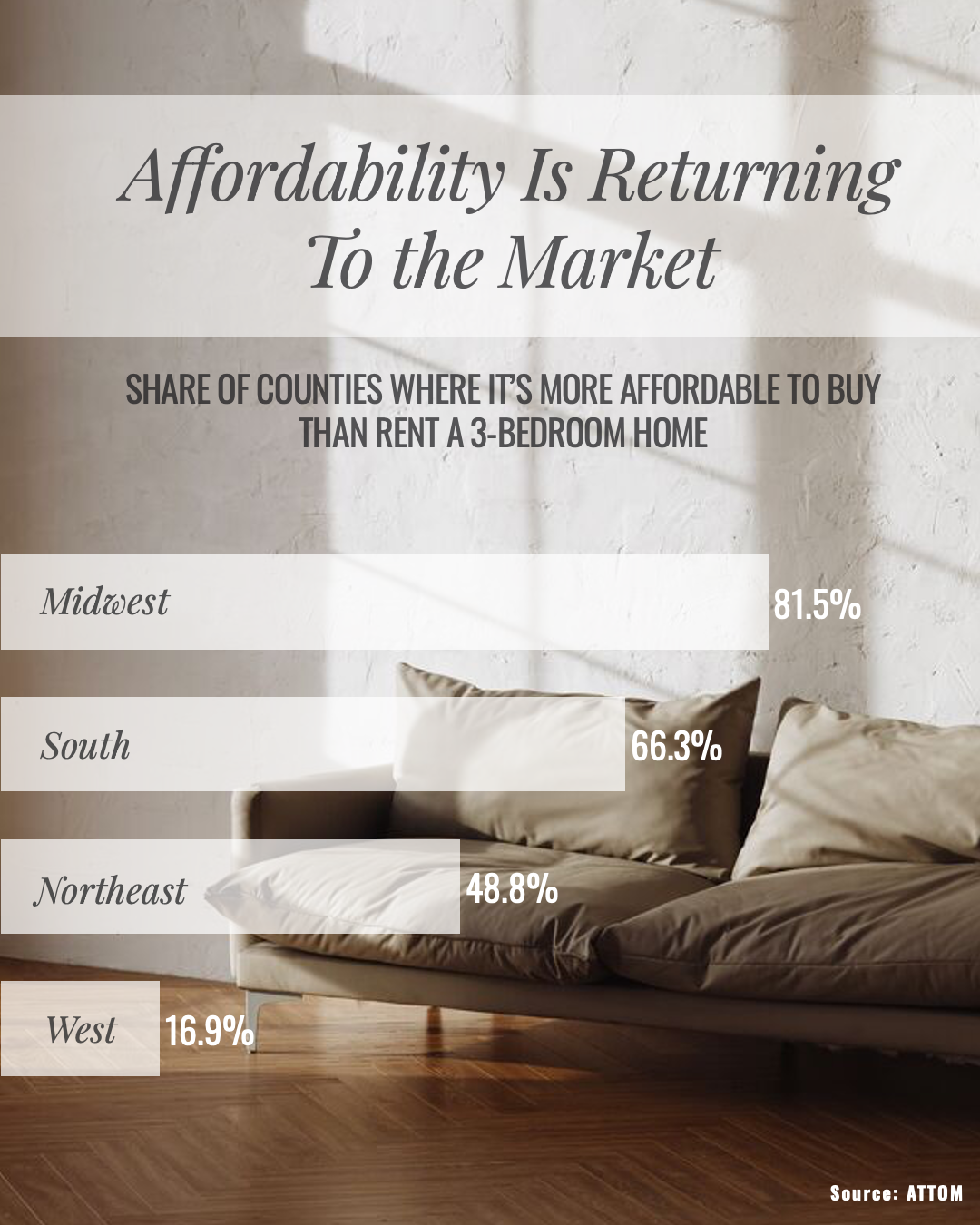

Affordability Is Returning To The Utah Market

Renting vs. Buying: The Numbers Might Surprise You Renting can feel like the easier choice right now. There’s no big down payment. No dealing with surprise repairs. And no long-term commitment. But then your rent goes up again. And again. And suddenly the thing that...

Understanding Dementia and Your Loved One

Understanding Dementia and Your Loved One Learn about their specific diagnosis (Alzheimer’s, Lewy body, vascular, frontotemporal) so expectations and plans match the condition and stage. Accept that changes in memory, behavior, and personality are caused by brain...

Top 2026 Housing Markets for Buyers and Sellers

Top 2026 Housing Markets for Buyers and Sellers Who doesn’t love a top 10 list? Well, here are two top 10 lists for the housing market this year. But before you take a look, there’s something you should know. If a move is on your radar for 2026, here’s the most...

January Buyers

You may not want to put your moving plans into hibernation mode this winter, because the savings this time of year are real. LendingTree found January buyers paid about $23k less than May buyers for the same size home. And that’s largely because the price per square...

Doug and Camille – Google Review

Marty & Laurie Gale are the Prince & Princess of Patience & Problem Solving when it comes to real estate! Not only did they help find the perfect buyer for our home, they also went the extra mile in getting us the right new home for us that enabled me to...

1 Million Reasons To Buy a Home

Buy or Sell with Marty Gale "Its The Experience" Principal Broker and Owner of Utah Realty™ Licensed Since 1986 CERTIFIED LUXURY HOME MARKETING...

How To Stretch Your Options, Not Your Budget

How To Stretch Your Options, Not Your Budget One of the biggest homebuying advantages you can give yourself today is surprisingly simple: a flexible wish list. Think of it like this. Your wish list and your budget are the guardrails of your search. And when your...

Why Selling Your House This Winter Gives You an Edge

Why Selling Your House This Winter Gives You an Edge Spring gets all the attention, but it’s not always the best time to sell a house. Yes, more buyers show up, but so do a lot of other sellers. Winter is different. With fewer homes on the market, your house has a...